Author: Riccardo Sozzi Reviewer: Zi Yi Sun

China is a unique case in global investment because it combines the scale of a major market with the structure of a partly state-directed economy. It is the world’s second-largest economy, yet household savings remain unusually high, financial markets are still shaped by policy intervention, and investment choices are split between bank deposits, property and a fast-evolving equity market. At the same time, “China” is everything but just one market: mainland exchanges, Hong Kong listings and overseas shares all matter. This mix of size, state influence and fragmented capital markets makes China unlike either the US model of market finance or the European one of bank-led stability.

Chinese households are still savers first and investors second. The World Bank estimates that the household saving rate stood at 35% of disposable income in 2023, a level shaped by ageing, gaps in the social safety net and weaker confidence after the property downturn.

Households save heavily partly for structural reasons: the World Bank and IMF both point to precautionary saving linked to healthcare, pensions, education costs and an uneven social safety net. That helps explain why Chinese households still prefer deposits, property and other lower-risk stores of wealth over riskier financial assets. PBOC depositor surveys in 2025 showed that more than 62% of respondents preferred to save rather than spend or invest.

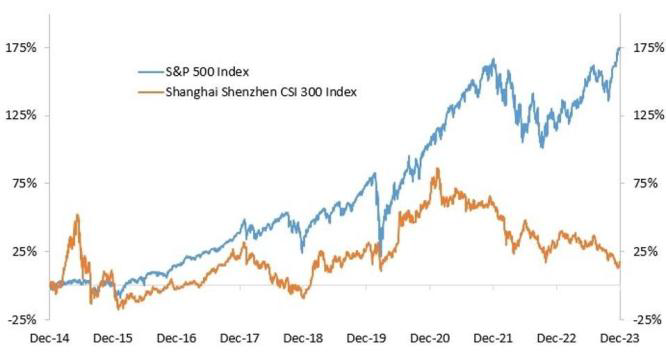

That caution is visible in where money goes. Housing remained the largest asset on household balance sheets in 2022, accounting for 47% of total household assets, while deposits made up 23%; equities and investment funds were much smaller at approximately 15%, with insurance and bonds playing a more limited role. And investing in equities has been no thrill for those few people: the Chinese stock market has returned much less than others. This can be partially explained by the fierce competition among Chinese corporations and the consequent run to cut prices.

Return on China CSI 300 Index vs. US S&P 500 Index

Source: Bloomberg

Finally, it’s interesting to note that even if China is climbing general education rankings, the country ranks below advanced economies in global financial literacy surveys. Around 28% of adults meet basic financial literacy standards, compared with over 50% in most developed countries, placing China closer to emerging-market averages than to Western benchmarks.

As said before, China’s stock market is not one market; in fact, it’s a linked system of three. In mainland China, Shanghai is the core domestic exchange, focused on large companies and home to the STAR Market for tech firms, while Shenzhen is more oriented towards smaller and fast-growing businesses through its ChiNext board. Hong Kong plays a different role: since the launch of Stock Connect in 2014, it has become the main bridge between China and global investors, offering a more open and international market. Compared with Western markets, mainland trading is more tightly controlled, with daily price limits that help contain volatility. Even so, Chinese equities are often more volatile and driven by sentiment. This is largely due to the strong presence of retail investors, who trade frequently and react quickly to market trends.

At the same time, authorities are trying to rebalance the market. Policymakers have been encouraging greater participation from institutional investors such as pension funds and insurers to improve stability and promote long-term investment.

Regulation and taxation are part of this system. The state plays an active role in supporting markets and guiding capital flows. Capital gains on listed shares are effectively tax-free for individual investors, while dividends are taxed depending on the holding period. In 2023, the government also cut stamp duty on stock trading to support activity. Hong Kong follows a simpler model, with no capital gains tax but a small stamp duty, reinforcing its role as China’s most international financial center. This is pushing more retail and institutional investors towards the Equity market.

However, this recent shift in China should not be interpreted as a sudden move towards risk, but rather a clear weakening of property as the dominant investment. Official data show real estate investment fell 17.2% in 2025, with new starts down 20.4% and the value of new-home sales down 12.6%. After years of rapid growth, the real estate sector has slowed sharply, pushing many households to reconsider where to put their money. Interest in financial assets is starting to pick up, although still gradually. In particular, exchange-traded funds (ETFs) and the Hong Kong market have attracted growing attention, helped by easier cross-border access and a wider range of investment options.

This does not mean China is becoming a US-style equity culture overnight. Property and bank deposits still account for a large share of household wealth. However, the direction of change is becoming clearer. More savings are slowly moving into financial markets.

The World Bank still describes housing as the dominant household asset in China and bank deposits as the second-largest, while the IMF says the financial system remains bank-centric and largely government-controlled. But policy is clearly pushing the market towards a stronger institutional base. A January 2025 plan from China’s financial authorities called for higher and more stable share allocations by insurers, social security and pension funds, longer performance-assessment cycles, and a bigger role for equity funds. That being said, to support this growth, the Chinese stock market must present better results in the future.

Looking ahead, the most likely scenario is a gradual shift rather than a rapid transformation. High savings, a still-dominant property sector and strong state involvement continue to shape household behavior, but gradual changes are underway. Financial markets are expected to grow in importance, institutions to become more influential, and products like ETFs to expand further. The evolution will depend not only on policy support, but also on market performance and rising financial literacy. At the same time, the state will remain a central player, shaping both the pace and direction of market development. China is not likely to converge toward a Western model, but developing its own hybrid system – one where markets grow in importance while the state remains firmly at the center.

Sources:

National Bureau of Statistics of China (NBS) — Investment in Real Estate Development for 2025, 20 gennaio 2026. stats.gov.cn — Verifica dati immobiliari (-17.2%, -20.4%, -12.6%)

Peterson Institute for International Economics (PIIE) — Does a Weak Social Safety Net Drive China’s High Savings?, Working Paper PB25-7, dicembre 2025. piie.com — Household saving rate 35% of disposable income (2023)

World Bank — Gross Domestic Savings (% of GDP) — China, World Development Indicators. data.worldbank.org — Gross savings rate 43.2% of GDP (2023)

World Bank — China Economic Update, dicembre 2025. thedocs.worldbank.org — Household saving drivers (ageing, safety net, property)

Bank for International Settlements (BIS) — Working Papers No. 1319: Housing Wealth Effects in China. bis.org — Quote PBOC 2019 survey: housing ~70% of urban household assets

S&P Global / World Bank — Financial Literacy Around the World (Findex/FinLit Survey) — 28% adult financial literacy baseline for China

CEIC / Center for National Balance Sheets — National Balance Sheet Accounts 1978-2022: Household. ceicdata.com — Asset breakdown 2022 (deposits, equity, total)

GAM Investments — China Housing Market Downturn and Its Impact, 13 gennaio 2026. gam.com — Contesto property crisis e equity market

KPMG — China Economic Monitor Q3 2025, agosto 2025. kpmg.com — Real estate investment data mid-2025

0 Comments